India’s national digital health initiative, now known as the Ayushman Bharat Digital Mission, is designed to create a unified, interoperable digital health ecosystem. At its core is the Health ID, officially called the Ayushman Bharat Health Account or ABHA, which allows citizens to create and manage digital health records and share them securely with healthcare providers and other authorised entities. As the system matures, one of the most frequently asked questions relates to how this Health ID can be linked with private health insurance policies to simplify verification, cashless treatment, and claims processing. This article explains the structure of the National Digital Health Mission, how the Health ID functions, and the verified ways in which it can be connected to private insurance, based strictly on officially notified frameworks and documented practices.

Background: What the National Digital Health Mission is and how the Health ID works

The National Digital Health Mission was launched to build the digital backbone of India’s healthcare system. It is overseen by the National Health Authority and operates as part of the broader Ayushman Bharat programme. The mission’s objective is to enable secure, standardised exchange of health information across public and private healthcare providers while ensuring that individuals retain control over their personal health data.

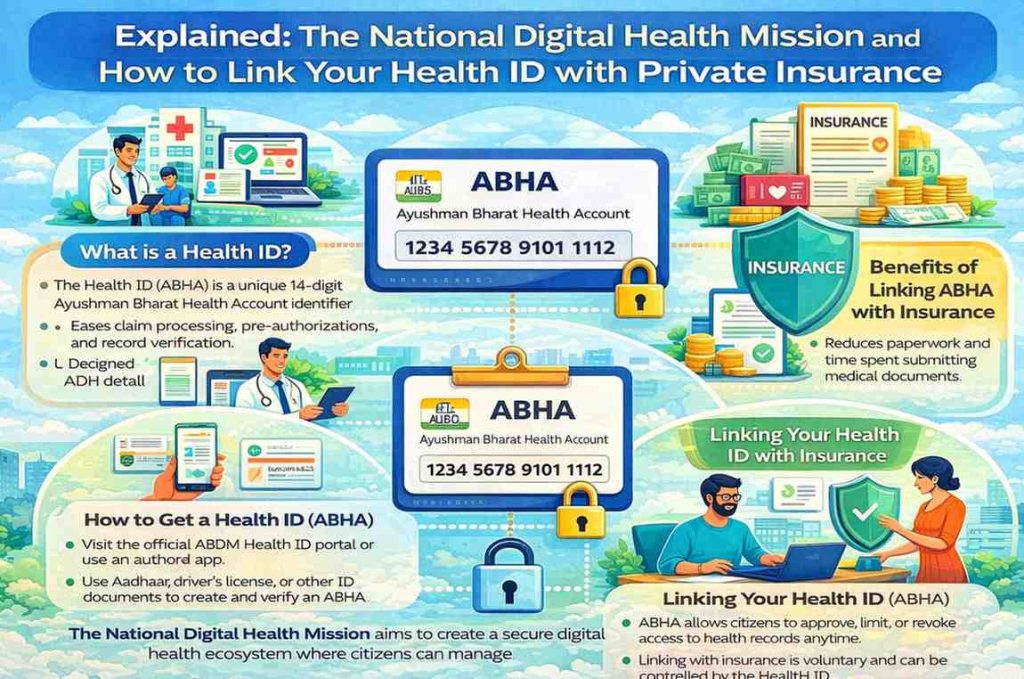

The Health ID, or ABHA, is a unique 14-digit number linked to a digital health address. It does not store medical records itself. Instead, it acts as a reference that allows health records generated by hospitals, clinics, laboratories, and diagnostic centres to be linked to an individual in a secure and consent-based manner. Medical data remains with the institutions that generate it and is shared only when the individual explicitly permits access.

Participation in the Health ID system is voluntary. Citizens can create an ABHA using Aadhaar or other accepted identity documents, along with mobile number verification. The system is designed to allow individuals to access their records digitally, share them when required, and withdraw consent at any time.

The digital health architecture behind record sharing

The National Digital Health Mission operates through a defined digital architecture that assigns clear roles to participants. Healthcare facilities and systems that generate and store medical records function as Health Information Providers. Entities that seek access to those records, such as hospitals involved in follow-up care or insurers processing claims, act as Health Information Users.

A key feature of the system is the consent manager, which ensures that data flows only after explicit approval from the Health ID holder. When an organisation requests access to records, the individual receives a consent request specifying the purpose, type of data, and duration of access. Only after the individual approves this request does the system allow data exchange.

This consent-first model is intended to ensure transparency and accountability. Every transaction is logged, and access is restricted to the scope approved by the user. These technical and operational principles are central to the mission’s design and are meant to safeguard individual privacy.

Why private insurers are engaging with the Health ID system

Private health insurers operate in an environment that requires verification of medical history, diagnosis, and treatment details for underwriting, pre-authorisation, and claims settlement. Traditionally, this process relies heavily on paper documents, repeated submissions, and manual verification, often leading to delays and disputes.

The Health ID offers insurers a way to access verified medical records in digital form, subject to policyholder consent. When implemented correctly, this can reduce administrative delays, improve accuracy in claims assessment, and simplify the experience for policyholders who would otherwise need to submit multiple documents.

Insurers that support Health ID integration generally describe it as a facilitative tool rather than a mandatory requirement. The system is positioned as a way to streamline processes, not to replace existing regulatory checks or underwriting norms.

Creating a Health ID: what citizens need to know

Creating a Health ID is a relatively simple process. Individuals can generate an ABHA online through official portals or authorised applications, or through assisted modes at healthcare facilities. The process involves identity verification and mobile number authentication.

Once created, the Health ID can be accessed through digital platforms that allow users to view linked health records, manage consent, and update personal details. For individuals who are not digitally comfortable or lack internet access, assisted creation options are available at designated health facilities.

The Health ID remains under the control of the individual. It can be used selectively and does not require continuous or blanket data sharing with any organisation.

How Health ID linkage with private insurance works in practice

There is no automatic or centralised mechanism that links a Health ID with all insurance policies by default. Instead, linkage occurs through specific, consent-based interactions between the policyholder, the insurer, and, in some cases, the healthcare provider.

One common method is through insurer portals or mobile applications. Some insurers allow policyholders to add their Health ID to their policy profile. During this process, the policyholder is asked to authenticate their Health ID and grant consent for its use. The insurer may then use the Health ID as a reference during claims or service requests, subject to fresh consent for accessing records.

Another route is hospital-assisted linkage. When a policyholder seeks treatment at a hospital that supports the digital health ecosystem, the hospital may ask for the Health ID at the time of admission. With the patient’s consent, the hospital can link current treatment records to the Health ID and share necessary information with the insurer for cashless approval.

A third scenario arises during claims processing. Even if a Health ID was not previously linked to the policy, the claimant can provide it during claims submission and authorise the insurer to access relevant medical records for that specific claim. This consent is typically limited in scope and duration.

What policyholders should expect during the linking process

When linking a Health ID with an insurance policy, policyholders should expect a consent-based authentication flow. This usually involves confirming identity details and approving specific permissions. The consent request clearly outlines what data can be accessed and for what purpose.

Policyholders retain the right to revoke consent. Access is not permanent unless explicitly authorised, and insurers are expected to comply with data protection and confidentiality requirements.

The exact user interface and steps vary between insurers, but the underlying principle of explicit, informed consent remains constant across implementations.

Privacy, data protection, and user control

Concerns around data privacy are central to discussions about digital health. The National Digital Health Mission is built on the premise that individuals remain the owners and controllers of their health data. Records are shared only after consent, and only for defined purposes.

Healthcare providers and insurers participating in the ecosystem are expected to implement secure data storage, encryption, and audit mechanisms. They are also bound by existing legal and regulatory obligations governing personal and sensitive data.

While the digital architecture provides safeguards, effective protection also depends on organisational compliance and oversight. Users are encouraged to review consent requests carefully and remain aware of how their data is being used.

Limitations and current gaps in implementation

Despite its ambition, the digital health ecosystem is still evolving. Not all hospitals, clinics, and insurers are fully integrated with the system. As a result, the availability of end-to-end digital record sharing varies by region and provider.

In many cases, paper documents and manual processes continue alongside digital workflows. The Health ID does not automatically retrieve all past medical records, particularly if those records were generated by facilities that are not yet part of the ecosystem.

These limitations are part of an ongoing transition. The system is designed to expand gradually as more institutions adopt the required standards and infrastructure.

Practical considerations for citizens

Citizens interested in using their Health ID with private insurance should first ensure that their ABHA is created and verified. They should then check whether their insurer supports Health ID integration and understand the consent process involved.

During hospital visits or claims submission, providing the Health ID can help facilitate digital exchange where available, but individuals should remain prepared for hybrid processes that include manual documentation.

Maintaining awareness of consent settings and reviewing access permissions periodically is advisable to retain control over personal health data.

Impact on patients, insurers, and the healthcare system

For patients, the Health ID has the potential to reduce paperwork, improve continuity of care, and simplify insurance interactions. For insurers, it can enhance efficiency and accuracy in claims processing. For the healthcare system as a whole, it supports better data interoperability and long-term planning.

These benefits depend on widespread adoption, robust governance, and sustained trust among users. The mission’s success will ultimately be measured by how effectively it balances convenience with privacy and security.

Conclusion

The National Digital Health Mission represents a foundational shift in how health information is managed and shared in India. The Health ID is central to this transformation, offering individuals a way to organise and control their medical records digitally. Linking a Health ID with private insurance is possible through consent-based processes involving insurers and healthcare providers, but it remains voluntary and context-specific.

As adoption grows, the integration between digital health records and insurance services is expected to become smoother and more widespread. For now, citizens who choose to participate should do so with a clear understanding of consent, privacy, and the practical limits of the system.

Add digitalherald.in as preferred source on google – click here

Last Updated on: Thursday, January 29, 2026 10:38 am by Digital Herald Team | Published by: Digital Herald Team on Thursday, January 29, 2026 10:38 am | News Categories: India